This Stock Loves Volatility—Up 50% and Still Undervalued

In this deep dive, we explore how Flow Traders profits from panic, operates behind the scenes of global markets, and quietly crushed benchmarks by staying out of the spotlight.

We added FLOW to the portfolio at its inception and haven’t made a single change since. It’s been about around 6 months, and the stock is up nearly 50%.

Flow Traders: Liquidity, Volatility, and the Art of Market Making

In the spring of 2020, as global markets convulsed in pandemic panic, a little-known Dutch trading firm quietly racked up record profits. While most investors saw chaos, Flow Traders saw opportunity – its profits in 2020 surged more than 8 times year-on-year. This dramatic windfall wasn’t a one-off fluke, but rather a showcase of Flow Traders’ core strength: thriving on market volatility. In this deep dive, we explore Flow Traders (Euronext: FLOW) through a long-term, value-oriented lens – examining its business model, competitive moat, financials, leadership, and how it stacks up against high-speed trading rivals like Virtu and Citadel. Buckle up – it’s time to “go with the Flow.”

In this article you will read;

Business Overview: What Does Flow Traders Do?

Economic Moat and Industry Landscape: How Durable is Flow’s Edge?

Financial Health: Volatile Income, Solid Balance Sheet

Management and Governance: Skin in the Game and Strategic Shifts

Capital Expenditure: Light Investments with High Returns

Sector Cyclicality and Structural Tailwinds: Riding the Waves

1. Business Overview: What Does Flow Traders Do?

Flow Traders is a global technology-enabled liquidity provider – in plainer terms, a proprietary trading firm that makes markets in financial instruments. Founded in Amsterdam in 2004 by two Dutch traders, the company has grown into one of the world’s largest market makers for exchange-traded products (ETPs). Flow continuously quotes bid and ask prices on thousands of securities, profiting off the small spread in between. Its bread-and-butter is ETPs (like ETFs and ETNs), but it has diversified across asset classes including equities, commodities, bonds, currencies, and even digital assets like crypto.

Products & Services: The firm’s product coverage is vast. It provides liquidity for over 13,000 ETP listings globally, from plain-vanilla stock index ETFs to commodity and fixed-income ETPs. In recent years Flow Traders also branched into cryptocurrencies, becoming an early mover in making markets on crypto exchanges starting in 2019. Additionally, it trades individual equities, equity options, foreign exchange, and fixed income products – essentially any electronic market where it can narrow the bid-ask spread and earn a turn. It does not have external clients in the traditional sense (it’s not a broker or asset manager); rather, its “service” is to provide continuous two-sided quotes and deepen market liquidity. For this service, Flow sometimes earns rebates or fees from venues and issuers, but primarily it earns trading profits (Net Trading Income) from buying slightly below and selling slightly above fair value.

Customers and Counterparties: Flow’s counterparts are the myriad of investors and traders transacting in the markets. When a retail investor buys an ETF on an exchange, or an institution unloads a block of bonds via an electronic platform, Flow Traders may well be on the other side of that trade, taking the other side and later offsetting the risk. In essence, every market participant is a potential counterparty. Flow also partners with ETF issuers as an Authorized Participant, helping create or redeem ETF shares to keep prices in line with underlying assets. Its “customers” are the markets themselves – by stepping in to buy when others are selling (and vice versa), Flow provides valuable liquidity, tightens spreads, and enables large trades to occur efficiently. The firm operates globally with trading hubs in Europe (Amsterdam), the Americas (New York), and APAC (Singapore, Hong Kong), ensuring a 24-hour presence. This global footprint and always-on approach means Flow Traders can respond to volatility anywhere, anytime.

How Flow Makes Money: Flow is a proprietary trading firm, meaning it uses its own capital (no outside AUM) to trade. Its income comes from Net Trading Income (NTI) – effectively the aggregate trading profits it earns across thousands of small trades. If markets are active and spreads are wider (e.g. during turbulence), NTI tends to surge. In calmer periods with tight spreads and low volume, NTI shrinks. Crucially, Flow does not take big directional bets; it tries to remain market-neutral, focusing on short-term price dislocations. The business is highly scalable: once its trading infrastructure and algorithms are in place, higher trading volumes translate directly into higher income with minimal incremental cost. This scalability was on full display in 2020 and again in late 2024, when volatility spiked and Flow’s revenues exploded (more on that in the next section).

In summary, Flow Traders functions as a market’s shock absorber – providing liquidity and absorbing temporary supply/demand imbalances. It’s paid in trading profits for bearing short-term risk and enabling other investors to move in and out of positions efficiently. As we’ll see, this model yields very uneven revenues (feast-or-famine based on volatility) but has produced outstanding long-term growth since inception.

2. Economic Moat and Industry Landscape: How Durable is Flow’s Edge?

Flow Traders operates in a fiercely competitive arena of high-frequency trading (HFT) and market making. Its main rivals are specialized trading firms like Virtu Financial, Citadel Securities, Jane Street, IMC, and others – an exclusive club of fast and well-capitalized players. In this landscape, speed, technology, and scale form the critical moats. Let’s break down Flow’s competitive positioning and the industry dynamics:

Competitive Landscape: In the ETP liquidity space, Flow Traders is a market leader in Europe and aims to be top-5 in the U.S. (Flow Traders). It faces competition from proprietary trading giants: U.S.-based Virtu (publicly listed) and Citadel Securities (Ken Griffin’s market-making behemoth) are larger by revenue, and private firms like Jane Street and IMC also command significant share in various markets. For perspective, Citadel Securities reported an astonishing $9.7 billion in trading revenue in 2024 – roughly 20 times Flow’s scale – and a net income of $4.2 billion (Citadel Securities - Wikipedia). Jane Street (another private firm) is similarly massive, reportedly hauling in $8.4bn revenue in just the first half of 2024 (Why Jane Street should pay more than Citadel Securities & both ...). Virtu, a closer peer to Flow, had $1.822bn in net trading income in 2024 (Virtu Announces Fourth Quarter 2024 Results). By contrast, Flow’s 2024 NTI was €467.8m (≈$515m) (Flow Traders 4Q and FY 2024 Results). Clearly, Flow is smaller in absolute terms than some U.S. rivals, but it has carved out a strong niche in ETPs and is expanding into new asset classes to close the gap.

Moat – Technology & Infrastructure: Flow Traders’ primary moat is its proprietary trading technology platform. The firm has invested heavily in a “leading edge, scalable” system that can price thousands of instruments in real-time and execute across dozens of venues with minimal latency. This technology – including co-located servers, fast algorithms, and smart order routing – is a major barrier to entry. Only a handful of firms in the world can compete at this level of speed and sophistication. Flow’s tech allows it to quote competitively tight spreads; in many less-trafficked ETPs, it might be the sole or primary market maker, giving it pricing power in that it can earn a slightly larger spread where competition is thin. The platform is also highly scalable – evidenced by Flow’s ability to handle surges in volume without skipping a beat (e.g. trading €1.545 trillion in ETP value in 2024.

Scale & Global Reach: Scale begets advantages in this industry. Flow’s presence across three regions means it can seamlessly transfer risk around the globe and capture opportunities in any time zone. Its trading capital (the firm’s own capital at risk) has grown to €775m as of end-2024, providing a solid base to support large trading positions. While smaller than Virtu or Citadel’s war-chests (Citadel’s trading capital was $16bn by end of 2024), Flow’s capital is ample for ETP market making. Economies of scale exist in terms of technology development (one algorithm can be used in many markets) and market access (Flow connects to 180+ trading venues). There’s also a network effect: Flow’s strong reputation and relationships help it secure memberships on exchanges, partnerships with new platforms, and invitations to provide liquidity in new products (for example, it’s partnering with platforms like AllUnity for 24/7 digital asset trading). These factors make it hard for a new entrant to unseat Flow Traders in its core niches.

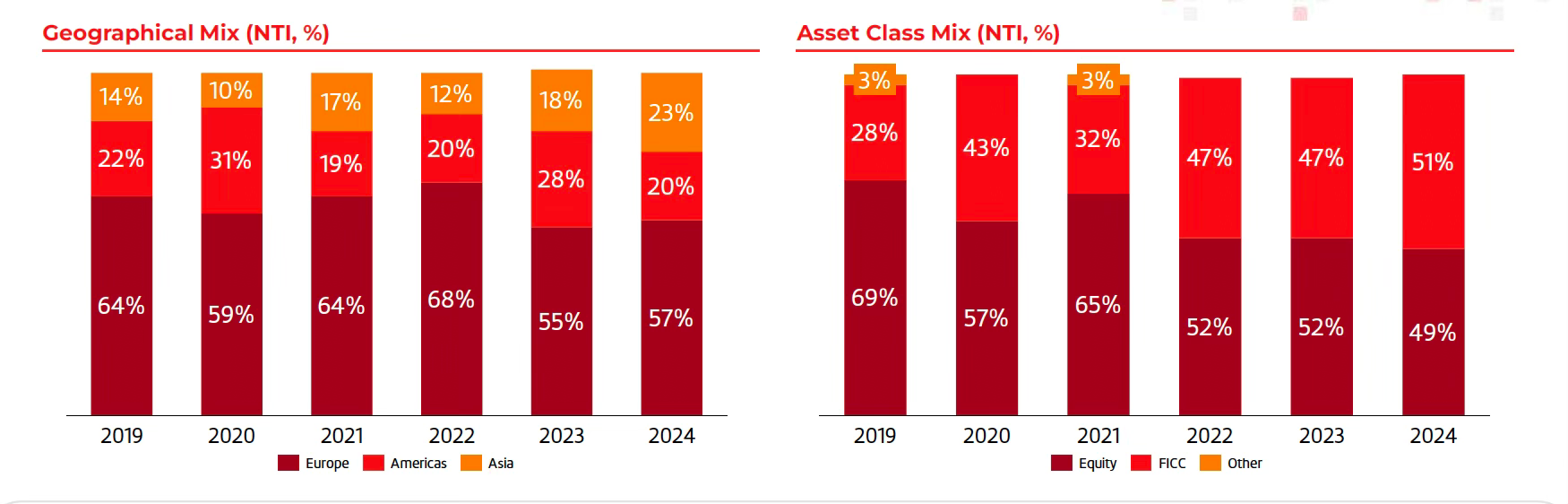

Diversification as Moat: A key strategic theme for Flow is diversification of asset classes, which management sees as critical for “structural growth”. Originally an ETF specialist, Flow has expanded into fixed income ETPs, currencies (FX), and crypto. This not only opens new revenue streams but also smooths out cyclicality. For instance, if equity market volatility is dormant, perhaps FX or crypto markets are active – Flow can earn income there. In 2024, volatility and volumes increased meaningfully in Asia and digital assets, and Flow’s multi-asset reach enabled it to capitalize. Its CEO highlighted that multi-year investments in Asia and crypto paid off in 4Q24, allowing Flow to profit from dislocations across regions and asset classes. This diversification enhances the durability of its competitive advantage by making the business less one-dimensional than in its early years.

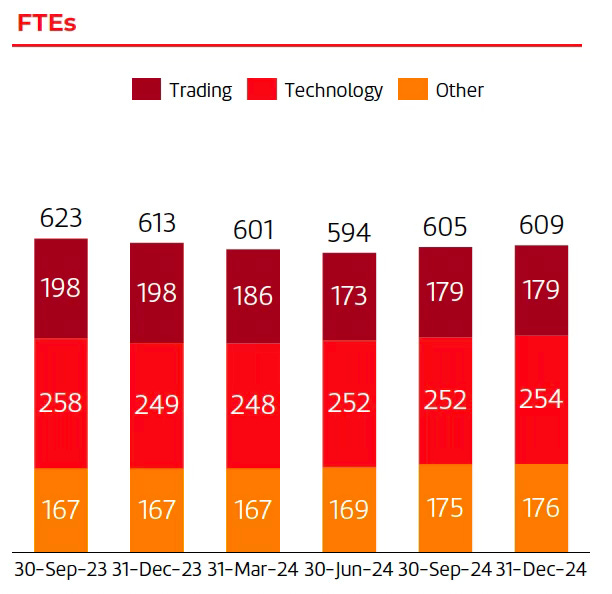

Durability of Competitive Advantages: The big question – can Flow’s edge last? In high-frequency trading, there is always the risk of technological obsolescence – today’s speed advantage can become tomorrow’s baseline. Flow must continuously invest to stay at parity or ahead. The good news is that it has recognized this need: fixed operating expenses are guided to rise in 2025 due to “additional technology investments and targeted hires” in growth areas. This suggests Flow is not resting on its laurels. Another point of durability is human capital – Flow’s team of 600+ FTE includes top quantitative traders and engineers, and the firm has a culture of innovation (they even have a venture capital arm, Flow Traders Capital, to invest in financial market infrastructure startups). The long tenure of its success (20 years and counting) and retention of founding shareholders on the board indicate a stable, experience-backed operation.

Industry Trends – Tailwinds and Headwinds: Structurally, several trends favor Flow Traders. Passive investing growth means more assets in ETFs – global ETP assets and trading volumes have been rising, a positive for Flow which is a major ETF liquidity provider. In fixed income, electronification is underway (bonds trading on screen like stocks), and Flow is actively promoting this to carve a top-3 position in fixed income ETPs. The firm is also leveraging its infrastructure to become a notable player in FX (aiming for top-15 globally in Euromoney’s FX rankings). And of course, digital assets gaining institutional acceptance could open an entirely new frontier – Flow sees itself as a “bridge” connecting 24/7 crypto markets with traditional finance. Partnerships with crypto firms (like one with Galaxy Digital and DWS called AllUnity) position Flow to shape this emerging market.

Risks – Cyclicality & Competition: Despite its strengths, Flow Traders faces significant risks. The cyclicality of its earnings is the most obvious – the company relies on volatility and trading activity, which are largely outside its control and can swing widely. In a prolonged calm market, Flow’s revenues can shrink dramatically, as seen in 2019 and 2023 when NTI fell to very low levels (we’ll quantify this in the next section). Another risk is regulation: market makers face potential regulatory changes (for example, bans on PFOF – payment for order flow – or financial transaction taxes) that could adversely impact trading volumes or profitability. While Flow doesn’t rely on PFOF like some U.S. brokers, any market structure change that reduces off-exchange trading or imposes fees on trades could indirectly crimp its activity. Competition risk is also ever-present – heavyweights like Citadel Securities or Jane Street aren’t standing still. It’s noteworthy, though, that market making isn’t a zero-sum winner-take-all; multiple firms can thrive, and Flow has coexisted profitably alongside its larger peers by focusing on segments where it excels (ETPs, niche markets, etc.). Finally, switching costs in this industry are low from the perspective of trading counterparties – if Flow disappeared, other market makers would fill the gap fairly quickly. This means Flow must remain on top of its game; its continued success is a function of execution rather than customer lock-in.

In sum, Flow Traders’ moat rests on technological excellence, multi-asset reach, and accumulated expertise. It has proven capable of riding industry tailwinds (ETF growth, market electronification) while weathering competitive pressure. The firm’s advantages are durable but not unassailable – sustained reinvestment and innovation are required to keep the moat intact. The next sections will show how this translates into financial outcomes and how Flow manages its capital to uphold its edge.

3. Financial Health: Volatile Income, Solid Balance Sheet

Flow Traders’ financial profile can seem paradoxical: it’s highly profitable in the long run, yet its year-to-year results are extremely volatile. Long-term shareholders have enjoyed substantial cumulative earnings and dividends, but they must endure dry spells in between windfalls. Let’s dissect the key financial trends:

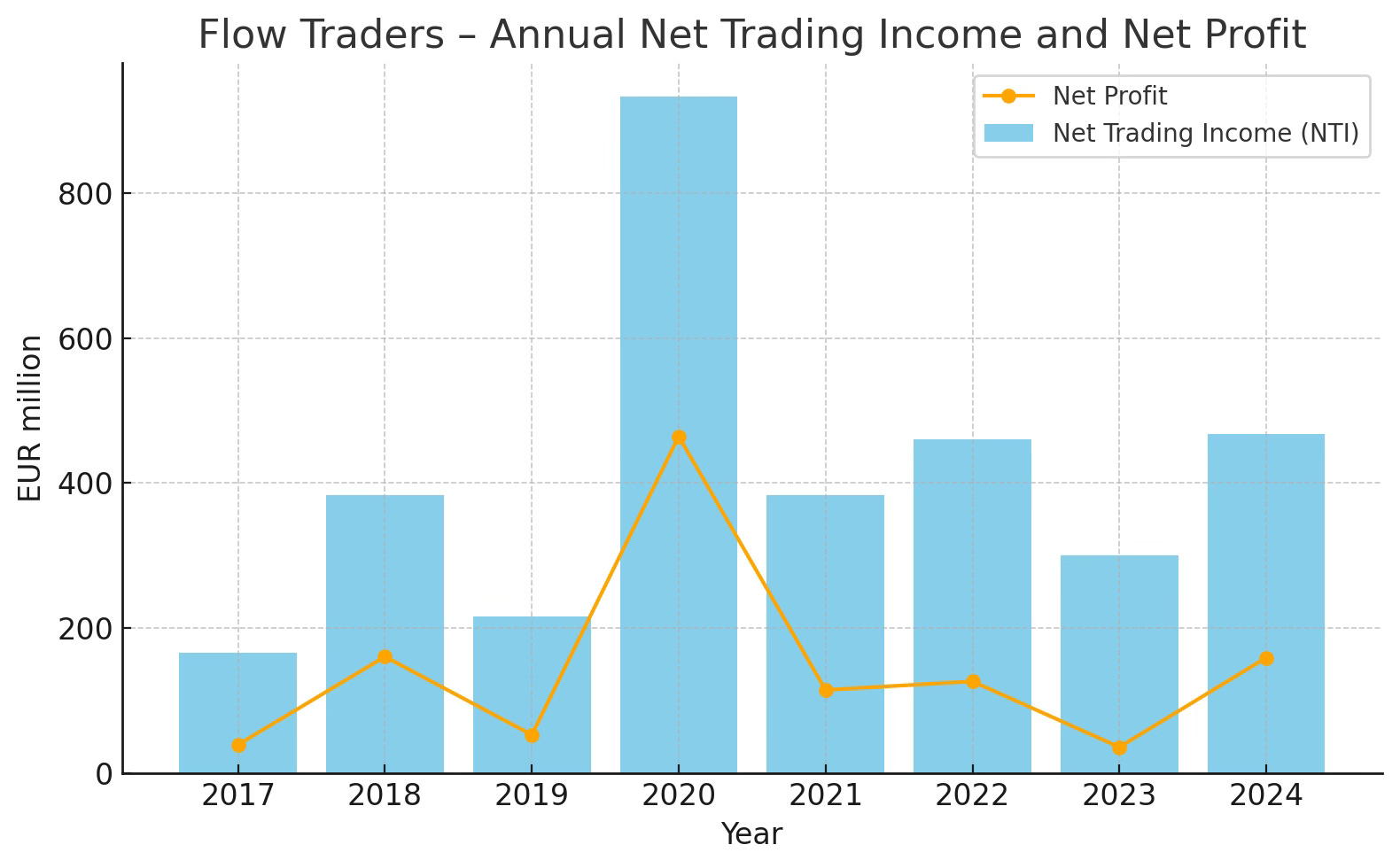

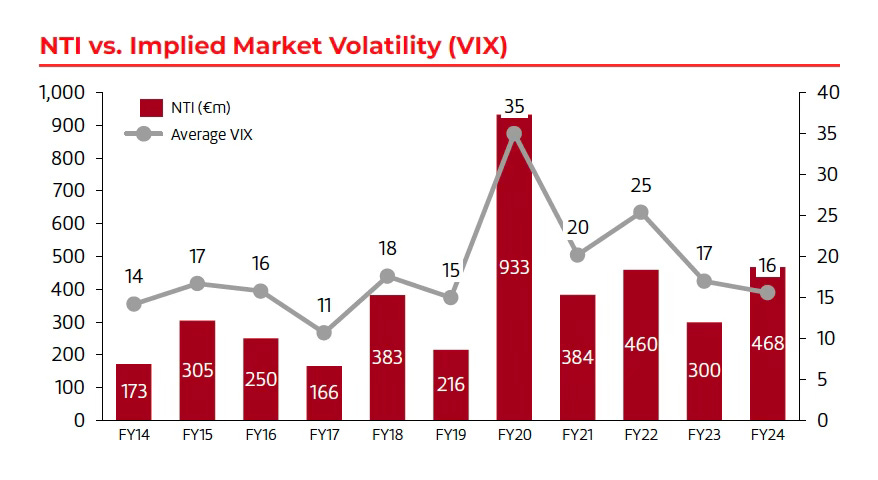

Revenue and Net Income Trends: Flow’s top line is its Net Trading Income (NTI), and it behaves like a rollercoaster aligned with market volatility spikes. The chart below illustrates this vividly – years of moderate income punctuated by occasional boom years when volatility soars:

As shown, Flow’s NTI hit a record €933 million in the turmoil of 2020 (up from just €216m in 2019) and net profit hit €464.5m that year. 2020 was an outlier driven by the COVID market shock. After the storm, 2021 saw a reversion to a modest €114.9m net profit as markets calmed. 2022 brought a mild uptick with €126.8m profit due to volatility (e.g. war in Ukraine). But 2023 was one of the calmest markets on record – Flow’s NTI fell to just €300m and net profit to €36.2m, the lowest in many years. Then, as if on cue, volatility resurfaced in late 2024 amid inflation and geopolitical tensions – Flow’s 4Q24 was its strongest quarter ever, capping a FY2024 NTI of €467.8m and net profit of €159.5m. That made 2024 the second-best year in company history (after 2020).

To normalize this, analysts often ask: what is Flow’s earnings power in a “typical” year? It’s tricky, but excluding extreme highs and lows, Flow might generate on the order of €100–€150 million in net profit in a middling volatility year. Indeed, from 2015–2019 (pre-COVID), net profits ranged €40–€161m, averaging ~€100m. The company itself has said it aims to structurally grow this baseline via diversification, but it’s safe to assume earnings will always be cyclical. Operating margins reflect this: in bonanza years, Flow’s EBITDA margins exceed 50% (62.8% in 2020; 45% in 2024) because revenues surge against a largely fixed cost base. In lean times, margins compress – e.g. ~22% EBITDA margin in 2023. Over a cycle, management believes a normalized operating margin in a more average environment is around 30–40%. For instance, 2022’s EBITDA margin was 45% (boosted a bit by some volatility) and 2019’s was ~36%. We’ll compare these margins to peers in the next sections – spoiler: Flow is competitive, if not superior, on profitability metrics relative to many rivals, despite its smaller scale.

Cash Flow and Capital Discipline: Given its earnings swings, Flow Traders has an admirably disciplined approach to capital. In fat years, the company gushes cash far in excess of its needs – for example, 2020’s free cash flow (net profit plus non-cash items) was well over €400m. Historically, Flow adopted a high payout policy, returning at least 50-60% of profits via dividends. In record 2020, it actually paid out 100% of net profit as dividends over the subsequent year (a total of €2.50/share relating to 2020 results). It also conducted share buybacks when it had surplus capital (e.g. a €25m buyback in 2022, and another €15m completed in Aug 2024). This generous shareholder return approach underscores management’s commitment to capital discipline – not hoarding cash unnecessarily.

However, a notable shift occurred in 2024: Flow suspended its dividend mid-year and instead raised additional capital (including taking on a small term loan) to fuel growth. This was part of a “Trading Capital Expansion Plan” aimed at seizing more opportunities in volatile markets. Essentially, management decided that reinvesting in trading capacity had higher returns than distributing cash at that moment – a sign of strategic flexibility. The result was trading capital increasing by €191m during 2024, giving Flow a much larger buffer to deploy in the next market upheaval. From a long-term investor’s view, this is a prudent move; it temporarily reduces cash yield (no 2024 interim dividend was paid) but potentially increases future earnings power (and thus future dividends) by allowing Flow to capture trades it previously might have passed up due to capital limits.

Even with the expansion, Flow’s balance sheet remains very solid. As of end-2024, shareholders’ equity (trading capital) was €775m. The firm carries minimal debt – by late 2024 it had roughly €50m in bank debt (management hasn’t disclosed the exact figure, but interest expense in 4Q24 was a mere €0.5m, implying a modest loan). It also holds substantial liquidity on the balance sheet (cash and equivalents, as well as positions that are mostly hedged and readily convertible). Regulatory capital requirements for market makers are relatively low; in fact, Flow had excess capital of over €110m above requirements even after 2018’s expansion, and similarly healthy buffers in 2019 (excess ~€133m) and 2024. The key point: Flow Traders is not financially leveraged – it does not need debt to operate and can easily withstand losses in any single trading day with its equity cushion. This conservative balance sheet approach is crucial in an industry where one bad bet with too much leverage can be fatal. Flow has never had a trading loss that imperiled its capital base.

Free Cash Flow (FCF) Yield: From a value investor perspective, Flow’s cash generation relative to price is very attractive – if one assumes through-cycle average earnings around €100m and that Flow will distribute most of that over time, the FCF yield is high. Indeed, based on 2024’s results and recent share price ~€27.4, Flow’s FCF yield is in the low double-digits (roughly 12–13%) – essentially reflecting its low earnings multiple (P/E ~7). Even taking a mid-cycle earnings of €100m, the stock trades at under 12x earnings, a yield of ~8–9%. We’ll detail this in the peer comparison, but it suggests the market heavily discounts Flow’s irregular earnings, perhaps providing opportunity for long-term holders who can ride out the volatility.

Operating Expenses and Efficiency: On the cost side, Flow Traders runs a lean operation. Fixed operating expenses in 2024 were €179m, up just 3% from prior year – demonstrating good cost control even as the firm grows. Variable costs (mainly bonuses to traders) fluctuate with profitability – e.g. in big years, compensation expense jumps (2024 total operating expenses +12% due to higher variable comp), but this is self-regulating and preserves margins. The firm’s fixed expense base primarily comprises personnel, technology, and office costs. Notably, headcount has been stable (609 FTE at end-2024 vs 613 a year prior), implying productivity gains as trading volumes rose 12% in 2024 with slightly fewer staff. Management frequently mentions “streamlining and automation” efforts to improve efficiency. In other words, they are aware that in quiet periods they need to keep costs in check – which they did in 2023, actually reducing certain costs to remain profitable even at low revenue.

Financial Solidity: To summarize Flow’s financial health: the company is profitable over the cycle, generates strong cash flows in volatile periods, and maintains a fortress balance sheet. Its weakest points are the lumpy earnings (which can make valuation tricky) and the reliance on external factors for revenue. However, it has proven capable of surviving droughts (it stayed in the black even in 2019 and 2023, albeit barely) and then thriving when conditions improve. Liquidity risk is minimal – Flow’s assets are largely cash or liquid securities, and it has no significant liabilities besides trade payables and a small loan. This financial robustness gives management the freedom to pivot – as seen by switching from paying maximum dividends to retaining capital when opportunities knock.

Looking forward, analysts forecast 2025 could be a more “normalized” year compared to 2024’s extremes. Flow itself guided fixed costs to rise to €190–210m in 2025 due to tech/talent investments, which implies it is preparing for further growth. Even if NTI were to regress somewhat (say closer to €300m again), Flow should remain solidly profitable given efficiencies. And any surprise spike in volatility (never say never) would be upside. For a long-term investor, the key is that Flow Traders has the financial resilience to endure the lean times and capitalize on the fat times – a hallmark of a well-managed cyclical business.

4. Management and Governance: Skin in the Game and Strategic Shifts

The human element behind Flow Traders is crucial – this is a company founded and led by traders, where savvy leadership can make the difference between seizing an opportunity or missing it. Let’s examine the management quality, track record, and how governance is structured:

Executive Team and Track Record: Flow Traders’ co-founders, Jan van Kuijk and Roger Hodenius, were instrumental in building the firm’s trading culture. They took the company public in 2015 and still remain significant shareholders (more on that shortly). While they are no longer in executive roles (both serve as Non-Executive Directors now), their presence has ensured continuity of the original vision. Day-to-day leadership is now in the hands of CEO Mike Kuehnel, who took the helm in early 2023. Kuehnel, notably, was the CFO since 2021 and comes from a finance background. His promotion to CEO after former CEO Dennis Dijkstra’s 14-year tenure signaled a new chapter. By all accounts, Kuehnel has hit the ground running – under his watch, the strategic pivot to retain capital for growth was executed in mid-2024, and Flow delivered a record-breaking Q4 2024. His CEO statement in the 2024 results exuded confidence, highlighting how the decision to boost trading capital led to capturing more opportunities and a 69% return on capital in 2024. It shows a willingness to make bold moves for long-term gain.

The broader executive committee includes Chief Trading Officer Folkert Joling (a company veteran) and recently a new Chief Technology Officer was nominated (Owain Lloyd, hired in 2024). This indicates an emphasis on technology leadership at the board level – a positive for a firm where tech is lifeblood. The mix of trading DNA and professional management appears well-balanced: traders drive the market strategies, while finance execs ensure discipline and investor communication. One can point to Flow’s steady cost management and shareholder returns as evidence that management isn’t just tech-savvy, but also financially prudent and shareholder-friendly.

Insider Ownership and Recent Trading: Founders Jan van Kuijk and Roger Hodenius own roughly 12.2% and 10.1%of Flow’s shares, respectively. Combined, over 22% of the company is in founder hands – a strong “skin in the game” signal. They have occasionally sold portions (notably a secondary sale in 2017 when private equity backer Summit Partners exited), but as of early 2025 they remain the two largest shareholders. Their stakes are described as long-term investments. There’s also a ~7.5% chunk of shares held as treasury (stock bought back, some of which is used for employee incentives). No other shareholder has more than ~3% (aside from Jupiter Asset Mgmt ~2.8%). This means insiders and employees collectively have a big influence. It also means management’s interests are well-aligned with public shareholders – they benefit primarily from stock appreciation and dividends. Recent insider trading activity has been quiet in terms of open market buys/sells (the founders last trimmed in 2017 as mentioned). The company itself, however, bought back shares in 2022–2024 (e.g. a €15m repurchase in 2024) and then allocated some of those treasury shares to employee bonus plans. This indicates a thoughtful approach: repurchase when stock is undervalued and use those shares to reward staff or reduce dilution.

Capital Allocation Strategy: Management has shown a clear framework for capital allocation:

Invest in Growth when justified: e.g. expanding trading capital in 2024 via retained earnings and modest debt – effectively reinvesting in the core business at what they believe to be high ROI (and 2024’s results vindicated that).

Return Excess to Shareholders: When capital levels are more than sufficient, Flow returns cash aggressively (dividends, special dividends, buybacks). For instance, after the blockbuster 2020, the company paid a €1.00 final dividend for 2020 on top of interim payouts, totaling a 75% payout, and later still had surplus to buy back shares.

Maintain strong Buffers: They keep a buffer above regulatory capital and a conservative debt profile. Even the new loan in 2024 is small relative to equity. Interest coverage is not an issue (interest expense was virtually nil historically, ticking up to just €0.5m in Q4 2024 after taking the loan) – EBITDA covers interest many dozens of times over.

This balanced strategy instills confidence. It’s neither a growth-at-all-costs approach nor a static return-everything approach, but rather dynamic based on conditions. The decision to suspend dividends in mid-2024 raised some eyebrows initially, but management communicated the rationale well and then executed by delivering higher profits with the deployed capital. That kind of credibility – doing what they said they would – speaks to management integrity and competence.

Cost Control: On the expense side, as mentioned earlier, management has kept fixed costs in line with guidance (2024 fixed costs €179m, “in-line with guidance” per results). They also scaled back hiring in soft periods (headcount was slightly reduced from 613 to 609 in 2024) even as they selectively added talent in growth areas. This shows they watch the bottom line closely – essential in a business where you can’t control the top line quarter to quarter. Notably, variable compensation acts as a buffer – it was 38% of operating profit in 2019 (a tough year) and naturally much higher in 2020 when profits exploded. By formula, this means in lean years payout ratios to staff shrink, preserving some profit for shareholders; in rich years, staff get a bigger piece but shareholders still win because the pie is huge. The comp structure thus aligns employees with performance, and management has not been shy about keeping that variable component truly variable (in 2023, bonuses would have been minimal given the tiny profit).

Leadership Initiatives: Under CEO Kuehnel, a few new initiatives stand out:

A Global Executive Committee was formed in 2022 to broaden leadership and execution on growth ambitions. This suggests a more institutional approach as the company scales (beyond a small founding team dynamic).

Increased focus on Asia-Pacific expansion – new offices (e.g. opening in Mumbai, expanding in Hong Kong and Singapore) and hiring record numbers of graduates in APAC. Kuehnel highlighted Asia as a region of meaningful volatility and opportunity in 4Q24.

Emphasis on partnerships and innovation – e.g. partnerships with Börse Stuttgart Digital, “Wormhole” (a digital asset bridge), and OpenYield (a fixed income platform). These are strategic moves to position Flow in nascent markets early, guided by leadership’s view of future trends.

All told, Flow Traders’ management appears high-caliber and aligned with shareholders. The founders’ ongoing stake and presence provide stability and a long-term outlook. The new CEO and team have demonstrated both offense(investing in growth areas) and defense (cost discipline) when each was needed. Governance mechanisms and transparency (regular trading updates, pre-close calls, etc.) are solid for a mid-cap company. If one were to nitpick, perhaps investor communications could further help the market appreciate Flow’s normalized earnings power – the stock’s low multiple suggests investors still get nervous about the dry spells. But management can only do so much talking; ultimately, delivering results and prudent stewardship will speak loudest. In that regard, the past years give us confidence that Flow Traders is in capable and shareholder-friendly hands.

5. Capital Expenditure: Light Investments with High Returns

Flow Traders is an asset-light business – its main “capital assets” are its trading software, hardware (servers/networks), and offices. Unlike a manufacturer or even a high-frequency trading firm that builds its own data centers, Flow doesn’t have huge capital expenditure (capex) needs. Nonetheless, it does spend steadily to maintain and upgrade its trading infrastructure and to enter new markets. Let’s examine its capex patterns and plans:

Maintenance vs Growth Capex: The majority of Flow’s capex is essentially maintenance/upkeep of its technology platform. This includes buying new servers, switching to faster network equipment, and capitalizing some portion of internally developed software. There is also some office-related capex (furnishing new offices, IT equipment for new hires, etc.). Historically, these needs have been small relative to profits. For instance, in 2019 (a relatively normal year), total capex was about €3.7 million. In the volatile 2020, capex ticked up to ~€6.8 million (perhaps they accelerated some tech upgrades given the windfall profits). Even at €6–7m, that was only ~1% of 2020 revenues – peanuts. In recent years, as they’ve grown, capex remained modest: the 2021 Annual Report indicates capex in low single-digit millions per region. So maintenance capex to keep the lights (and fiber optics) on is very low, which means Flow’s free cash flow closely tracks its accounting profit.

What about growth capex? One could classify certain investments as growth-oriented: for example, expanding into a new region (setting up a Hong Kong office might require buying some new hardware there), or adding connectivity to a new exchange (maybe needing specific equipment or software development). However, these expenditures are also small scale. Much of Flow’s growth efforts (like hiring new traders, or increasing trading capital) don’t show up as capex – they show up in operating expenses or just as allocated capital. For instance, building out crypto trading capability might involve writing new code (some of which might be capitalized software) and buying some servers – again likely in the order of a few million euros or less.

In short, Flow Traders’ capex is almost entirely maintenance, with any growth capex being incremental and easily covered by operating cash flow. The firm does not need to build massive infrastructure for growth – one of the beauties of its business model.

Given this profile, Flow’s free cash flow conversion is excellent. In years of positive profit, >90% of net profit typically converts to free cash (since capex is so low). Even growth plans won’t change that dynamic much. It’s part of why they can pay high dividends when they choose – there isn’t a need to retain earnings for big capital projects (in contrast, say, to a semiconductor firm that must reinvest a large chunk).

6. Sector Cyclicality and Structural Tailwinds: Riding the Waves

The market making sector is notoriously cyclical. As we’ve detailed, Flow Traders’ earnings vacillate with volatility cycles. But these cycles can actually be a feature, not a bug, for long-term investors – especially if structural growth underlies the peaks and troughs. Let’s explore the cyclicality of Flow’s business and the structural tailwinds that could elevate its baseline over time.

Volatility Cycles: By design, Flow Traders prospers in high-volatility, high-volume environments. In periods of market stress or rapid change (think the volatility explosion of Feb–Mar 2018, the COVID crash of 2020, or late 2024’s interest rate swings), Flow’s trading desks are extremely active and spreads often widen (meaning higher profit per trade). Conversely, in placid markets with low volatility, trading volumes drop and spreads compress – a double whammy that causes Flow’s NTI to fall. These cycles often don’t correlate with the broader equity market direction. For instance, 2020 was terrible for most companies’ earnings but phenomenal for Flow. 2022 saw stock markets down and many companies hurting from inflation, but Flow had a decent uptick from the war-induced volatility. On the flip side, 2021 was a bullish year for stocks (S&P up ~27%) but relatively low volatility, so Flow’s results were muted.

For an investor, this cyclicality means Flow Traders can act as a hedge in a portfolio – it tends to earn more when many stocks and assets are in turmoil. Indeed, some investors hold names like Flow or Virtu as a form of “crisis alpha.” However, one must be ready for dry periods like 2017 or 2019 when nothing much happens in markets (volatility indices at rock-bottom) and Flow’s profits shrink. The good news is Flow has remained profitable even in the lowest volatility regimes – indicating resilience. The management’s diversification strategy (across assets and geographies) aims to ensure there’s always some pocket of volatility to serve. We saw evidence of this in 2023: while equity markets were eerily calm, Flow managed to scrape profits partly thanks to activity in crypto and certain regional markets.

Resilience Across Bull and Bear Markets: Flow Traders is market-direction neutral – it doesn’t matter if it’s a bull or bear market, what matters is activity. In fact, prolonged bull markets that are grinding and smooth (low VIX) are worst for Flow (e.g. 2017). Sharp bear sell-offs or abrupt corrections are very good (e.g. early 2018, 2020). Interestingly, Flow can also do well in sudden bull moves or rotation – any scenario with dispersion and volume (for example, the meme-stock frenzy in early 2021 briefly boosted volatility and volumes). The key is change. As such, Flow’s fortunes are somewhat uncorrelated to equity indices. This makes it a potentially valuable addition to a long-term portfolio – it’s a stock that might surge when others falter. Over the long run, one could argue that markets will periodically have bouts of volatility (that’s a near certainty), so Flow will have its days in the sun. The structural question is: are those bouts frequent enough and is the baseline level of trading activity rising?

Structural Tailwinds: There are several secular trends that favor Flow Traders’ business:

Rise of Electronic Trading: More asset classes are moving from phone/OTC trading to electronic platforms. Flow is an electronic market maker; the more venues it can connect to, the more markets it can make. For example, the ongoing electronification of bond trading (with ETF volumes as a proxy) hugely benefits Flow. The company is proactively supporting this trend – it was lead sponsor of a Fixed Income Leadership Summit and partnered with platforms to push e-trading in bonds. As bonds, swaps, and other traditionally OTC markets go electronic, Flow’s addressable market widens.

ETF Market Growth: ETFs continue to gain share in investors’ portfolios worldwide. Every new ETF launched is a potential new product for Flow to make a market in. The ETP Value Traded on exchanges is rising long-term (Flow’s ETP trading volumes grew +5% in 2024 to €1.545 trillion, even in a mixed market). More ETF trading = more business for Flow, even if volatility is average. The number of ETP listings has grown (13,000+ that Flow trades, and many are niche – often relying on dedicated market makers like Flow to provide liquidity. As ETF adoption penetrates emerging markets and new asset classes (e.g. recent launches of crypto ETFs, active ETFs, etc.), Flow stands to be a key liquidity provider.

Global Market Access: Flow has been expanding globally – it now has a meaningful presence in Asia-Pacific, which it calls a strong growth area. Asian markets (like India’s exchanges, where Flow got a Qualified Institutional Investor license in 2022, or the growth of ETF trading in China, etc.) represent new territory. There’s a structural trend of financial market development in Asia, and Flow is positioning to ride that wave. Already in 2024, Asia was ~23% of Flow’s revenue, up from ~18% a year before – a sign of that structural growth.

Digital Assets and New Instruments: The emergence of cryptocurrencies and digital asset trading is a potential game-changer in the long run. These markets trade 24/7 and are extremely volatile – tailor-made for a firm like Flow Traders. Flow was one of the first regulated firms in Europe to trade crypto, and it now provides liquidity on multiple crypto exchanges. As regulations evolve, if crypto trading becomes more institutional (for instance, if a Bitcoin ETF gets approved in the U.S., triggering more volume), Flow could see a structural uptick. Moreover, the skillset transfers – making markets in crypto options, for example, is akin to other options. Flow has also invested in a crypto trading platform (Thalex) and a DeFi platform (Paradigm’s DZX), indicating it’s forward-looking here. While crypto is volatile (with booms and busts), it’s likely here to stay, and its integration into mainstream finance could be a new structural tailwind for Flow.

Regulatory Environment: Interestingly, some regulatory changes can benefit firms like Flow. For example, during the GameStop saga in 2021, U.S. regulators discussed shortening the settlement cycle to T+1 or even same-day – faster settlement increases demand for liquidity provision and robust market making (as there’s less time for trades to naturally settle). Europe’s MiFID II regulations pushed more trading onto lit exchanges and transparency, which can help electronic market makers gain share from bank dealers. On the flip side, any onerous regulation on high-frequency trading could pose a risk (like if exchange fees rise for market makers or if there were ever a ban on market making in certain instruments – unlikely). Generally, Flow operates in a regulated, transparent manner(it doesn’t do the controversial payment-for-order-flow stuff that attracts political risk). This relatively clean profile means it might even gain market share if regulators curtail less transparent practices elsewhere.

Client/Counterparty Attitudes: As markets evolve, the acceptance of non-bank liquidity providers like Flow has grown. A decade or two ago, big institutions might have preferred trading with banks. Now, many realize firms like Flow or Virtu often provide better prices. This secular shift in mindset (fueled by liquidity shortages during crises where non-bank players stepped in) is an intangible tailwind for Flow – it’s now seen as a reliable liquidity partner by exchanges and trading venues worldwide. For example, Flow being chosen as the exclusive liquidity provider for certain new platforms (like the BondBloX bond ETF in the US, per company reports) shows the trust in its capabilities.

Handling the Down Cycles: Flow Traders cannot eliminate its cyclicality, but it has strategies to mitigate the downs:

Diversification, as discussed, means there’s always some action somewhere.

Cost flexibility: A large portion of expenses is variable (bonus pool), which shrinks in bad times, preserving capital. Also, if a downturn looks prolonged, Flow can trim hiring or other discretionary spend, which they have done.

Maintaining a strong capital base: This might seem counterintuitive, but by having ample capital, Flow can stay active (and even increase market share) during low-volatility periods when some competitors might withdraw or scale down. For instance, in 2019 some HFTs exited certain markets due to low profitability; Flow remained (albeit making little profit) but was then positioned to grab outsized share when volatility returned in early 2020. This willingness to stay the course through cycles is a competitive advantage. In the CEO’s words, the expansion of trading strategies and capital in recent years is “a result of the company’s growth and diversification strategy” that showed its value when 2024’s volatility hit.

Outlook: While it’s impossible to predict volatility spikes, one can be fairly certain that markets will not stay calm forever. Already in 1Q 2025, we’ve seen pockets of turbulence (e.g. uncertainty around central bank policies). Flow Traders doesn’t need a 2020-level event every year to thrive; even moderate upticks (like 2022’s or 2018’s) can make a big difference. Meanwhile, the underlying growth in volumes and new products provides a rising floor. Even in the very quiet 2023, Flow’s NTI of €300m was higher than the last quiet year (2019’s €216m) (), partly because the firm was active in more markets and products. This suggests that the baseline is rising gradually – so the “troughs” of the cycle are higher than before.

Investors should view Flow Traders in context: it is both a cyclical volatility play and a structural growth play on the modernization of trading. It requires patience and tolerance for earnings swings, but it rewards that with outsized dividends in good times and portfolio hedging properties in bad times. As electronic trading continues to penetrate finance, Flow’s opportunities expand. To use a surfing analogy, Flow Traders is positioned with its surfboard at the ready – it can’t create waves, but whenever a wave comes, it’s among the best at riding it. Over a long horizon, the combination of many small waves and a few big ones can carry Flow (and its investors) far forward.

Final Thoughts: Flow Traders may not be a household name on par with big banks, but in the arenas where it competes, it’s a remarkable gladiator. The company has turned market turbulence into an art form of profit, all while maintaining financial prudence and adapting to the evolving market structure. For retail investors with a long-term horizon, Flow Traders offers a unique proposition: exposure to the plumbing of the financial markets – earning returns from the very act of trading that underpins all other investing. It’s a stock that provides diversification benefits (performing in times others might not) and one tied to the inexorable growth of global capital markets.

There will be quiet months or years when Flow’s results underwhelm – that’s the price of admission for this ride. But as history has shown, periods of calm are invariably followed by storms, and Flow Traders has proven it can not only weather those storms, but profit mightily from them. With a capable management at the helm, a sturdy balance sheet, and multi-pronged growth strategy, Flow Traders is well set to keep “driving transparency and efficiency” in markets – and to keep rewarding those who sail along with it for the long run.

💬 What are your thoughts on Flow Traders' potential? Share your insights in the comments below! If you found this content engaging, please like, share, and subscribe — your support truly motivates me to continue creating quality content.